Shares of Snowflake(NYSE: SNOW) have been in the doghouse for the majority of 2024 as concerns regarding the data cloud platform provider’s slowing growth and expensive valuation have weighed on the stock, but its latest quarterly results have infused new life into this beaten-down technology company.

Snowflake stock shot up nearly 33% following the release of its fiscal 2025 third-quarter results (for the three months ended Oct. 31) on Nov. 20. Let’s see why that was the case and check if now is a good time to buy this technology stock in anticipation of more upside.

Are You Missing The Morning Scoop?Breakfast News delivers it all in a quick, Foolish, and free daily newsletter. Sign Up For Free »

Snowflake reported fiscal Q3 revenue of $942 million, an increase of 28% from the same quarter last year, driven by a 29% increase in its product revenue to $900 million. The company’s revenue was well ahead of analysts’ expectations of $897 million. Meanwhile, its non-GAAP earnings came in at $0.20 per share. Though that was lower than the year-ago period’s reading of $0.25 per share, its earnings were well ahead of the $0.15 per share consensus estimate.

The guidance was the icing on the cake. The midpoint of Snowflake’s fiscal Q4 product revenue forecast of $908.5 million was significantly higher than the $884.5 million analyst estimate. The company has also raised its full-year product revenue guidance to $3.43 billion, which would be a 29% increase over the prior year. It was earlier expecting product revenue to increase 26% in fiscal 2025 to $3.36 billion.

It has also increased its operating margin estimate to 5% from the prior expectation of 3%. Snowflake’s beat-and-raise quarter can be attributed to the growing adoption of the company’s data cloud platform, which is benefiting from the integration of artificial intelligence (AI) solutions. For instance, the company exited the third quarter with just over 10,600 customers, up 20% from the same quarter last year.

It also benefited from higher customer spending during the quarter, with the number of customers who have generated more than $1 million in product revenue for Snowflake in the trailing 12 months jumping 25% year over year to 542. More importantly, the company has been able to generate more business from its existing customer base, which explains why it has upgraded its margin guidance as well.

This can be gauged from Snowflake’s net revenue retention rate of 127% for the quarter. The metric compares the product revenue generated by the company’s customers at the end of a quarter to the revenue generated by the same customers in the year-ago period. A reading of more than 100% in this metric means that Snowflake’s existing customers have either adopted more of its solutions or increased their usage of its offerings.

This combination of robust growth in the company’s customer base and higher spending by customers explains why Snowflake’s revenue pipeline is improving at an incredible pace. It finished the previous quarter with $5.7 billion in remaining performance obligations (RPO), a massive improvement of 55% from the same quarter last year.

This metric refers to the total value of a company’s contracts that will be fulfilled in the future. So, the faster growth in RPO as compared to its revenue indicates that Snowflake’s top-line growth is likely to remain solid. It is also worth noting that Snowflake expects to recognize half of its RPO as revenue in the next 12 months.

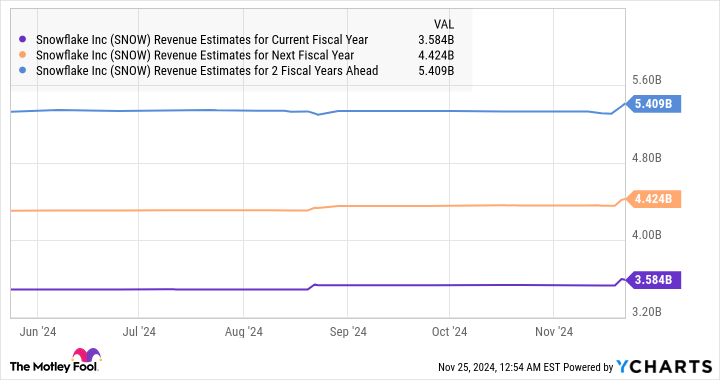

When compared to the $3.2 billion in revenue that the company has generated in the past four quarters, its RPO for the next 12 months means that it is well placed to deliver healthy revenue growth in the future. Not surprisingly, analysts have increased their growth expectations from Snowflake.

SNOW Revenue Estimates for Current Fiscal Year Chart

SNOW Revenue Estimates for Current Fiscal Year data by YCharts

At the same time, the company’s focus on integrating AI-focused solutions into its data cloud platform is also paying off. Snowflake has been offering multiple AI products to customers, with which they can build custom applications with the help of their proprietary data. On its latest earnings conference call, Snowflake management remarked that its AI and machine learning (ML) solutions have been deployed for more than a thousand use cases.

In all, more than 3,200 of Snowflake’s customers have already started using its AI offerings. That number could go higher as the company is focused on bringing more large language models (LLMs) into its ecosystem, which explains its partnership with AI company Anthropic. Snowflake customers will now be able to use Anthropic’s Claude 3.5 LLM to create generative AI applications, products, and workflows.

Snowflake’s latest numbers and guidance tick all the right boxes, but a closer look at the stock’s valuation could create doubts in investors’ minds. After all, Snowflake is trading at an expensive 16 times sales. That’s more than double the U.S. technology sector’s average price-to-sales ratio of 8. Also, we saw that the company’s bottom line shrunk last quarter, and analysts are expecting its earnings to drop to $0.70 per share in 2024 from $0.98 per share last year.

However, this bottom-line pressure can be attributed to Snowflake’s investments in AI-related infrastructure such as graphics processing units (GPUs). The company’s improved operating margin forecast for the current year indicates that its margins could start improving once again, which explains why analysts are expecting a nice jump in its earnings from next year.

SNOW EPS Estimates for Current Fiscal Year Chart

SNOW EPS Estimates for Current Fiscal Year data by YCharts

So, investors looking to buy a growth stock can consider buying Snowflake as its huge revenue pipeline and the potential jump in its earnings could help it justify its valuation — especially after its latest results, which indicate that its business is likely to accelerate.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $350,915!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,492!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $473,142!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of November 25, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.

Is Snowflake Stock a Buy Now? was originally published by The Motley Fool

Alisha Hunter is a news writer for Credence Advisors-News. She's been writing for over a decade, and she has taught herself all the skills she needs to be successful in this role.

Alisha has written about everything from technology to fashion; she's even written an advice column for brides-to-be!

Alisha loves reading books and watching movies - she's currently working on a book club with her friends where they read one book each month together!