The adoption of artificial intelligence (AI) technology is set to continue at a rapid pace in 2025: Market research firm IDC estimates that investments in data center infrastructure, AI agents, and efforts taken by organizations to embed AI capabilities into their operations will add up to outlays of $227 billion this year.

What’s worth noting here is that IDC expects 67% of that total to go toward businesses’ efforts to integrate AI into their operations. So 2025 could be a year of solid growth for both AI hardware and software companies. That’s why now would be a good time to take a closer look at two AI companies that could win big from the massive spending on AI infrastructure and solutions, and potentially see parabolic increases in their share prices.

A parabolic move refers to a sharp increase in the stock price of a company in a short period, tracing a path that resembles one side of a parabolic curve. Micron Technology(NASDAQ: MU) seems to be on that path — its stock price has risen 20% in 2025 already. Snowflake(NYSE: SNOW), too, has experienced a sharp jump in its stock price in recent months, and could very well maintain its momentum.

The memory market is expected to enjoy another year of solid growth in 2025 thanks to the AI trend. Market research firm Gartner estimates that unprecedented demand for high-bandwidth memory (HBM), which is used in AI accelerators to enable faster data transmission speeds and impart more computing power, along with increases in prices, could boost dynamic random access memory (DRAM) sales this year by 28% to $115.6 billion.

Micron is already making the most of the AI-driven opportunity in its core market. The memory specialist got a jump on larger rival Samsung, as it was Micron’s HBM chips that were selected for use in Nvidia‘s graphics cards for both gaming and AI workloads. More specifically, Nvidia’s upcoming GeForce RTX 50 series gaming graphics cards will use Micron’s HBM.

Meanwhile, Micron management announced on the company’s December earnings conference call that Nvidia’s Grace server CPU (central processing unit) is also using its HBM. Meanwhile, Nvidia picked Micron’s fastest HBM chip for use in its next-generation Blackwell AI systems. Samsung, on the other hand, has reportedly struggled to get its chips qualified at Nvidia, paving the way for Micron to keep making the most of the HBM market’s potential.

That bodes well for Micron, which forecasts that the size of the HBM market will grow from $16 billion in 2024 to more than $100 billion by 2030. At the same time, investors should note that Micron’s growth is set to pick up remarkably in its fiscal 2025 (which began Aug. 30). Revenue in the first quarter of the fiscal year increased by an impressive 84% year over year to $8.7 billion.

It also reported an adjusted profit of $1.79 per share as compared to a loss of $0.95 per share in the prior-year period. Analysts expect a 39% increase in Micron’s revenue in the current fiscal year to $35 billion, followed by another solid jump of 28% in fiscal 2026 to just under $45 billion. Additionally, Micron’s earnings are expected to jump to $8.90 per share in fiscal 2025 from just $1.30 per share in fiscal 2024, followed by a 44% increase in fiscal 2026 to $12.83 per share.

Based on these earnings estimates, Micron’s stock price could take off big time if it starts trading in line with the Nasdaq-100 index’s average forward earnings multiple of 26 (using the index as a proxy for tech stocks). Right now, Micron trades at just 13.6 times forward earnings. Investors, therefore, can get a great deal on this AI stock. Consider grabbing this opportunity before Micron soars higher.

Snowflake(NYSE: SNOW) saw impressive share price momentum since it released the results for its fiscal 2025 third quarter in November. Share prices jumped more than 23% since its quarterly report was released.

The company provides a data cloud platform that allows customers to securely consolidate data, which they can use to derive business insights and build applications. It also allows clients to share their data. For the period that ended Oct. 31, its revenue shot up by 28% year over year to $942 million. More importantly, Snowflake raised its guidance. It now expects its product revenue to rise by 29% to $3.43 billion in fiscal 2025.

However, don’t be surprised if Snowflake clocks even stronger growth in the new fiscal year (beginning next month). The company is seeing “significant adoption” of its AI-centric products, as management pointed out on the last earnings conference call. Management says more than 3,200 customers now use its AI and machine-learning features, which help employees perform tasks such as writing code and extracting data from documents. Given that Snowflake finished its last reported quarter with just over 10,600 customers, it still has a large opportunity to cross-sell its AI-focused offerings into its established user base.

Snowflake should be able to win a bigger share of its clients’ wallets from here — a pattern it has already established. In its latest reported quarter, its net revenue retention rate stood at an impressive 127%. This means that, on average, Snowflake’s existing customers spent 27% more on its offerings than they did in the year-ago period.

The stronger spending by existing customers, as well as a 20% year-over-year increase in its overall customer base, explains why Snowflake’s remaining performance obligations jumped by an impressive 55% to $5.7 billion. A company’s remaining performance obligations are the total value of its unfulfilled contracts, so the fact that this metric grew faster than revenue last quarter suggests that Snowflake’s future could be even brighter.

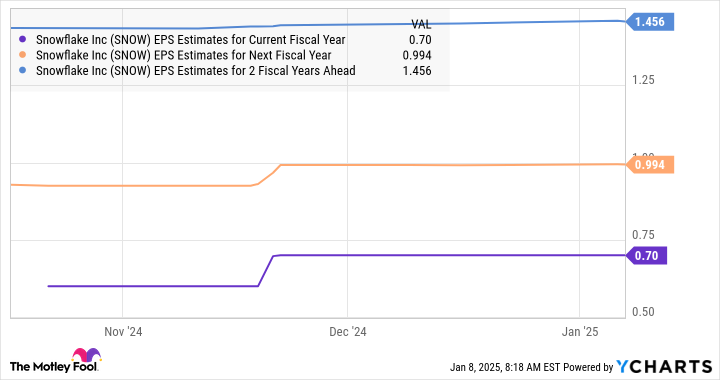

Moreover, analysts’ consensus estimates are for a 42% jump in Snowflake’s earnings in fiscal 2026 to $0.99 per share, and that’s expected to be followed by even better growth in the following year.

Data by YCharts.

As such, Snowflake is likely to remain a top growth stock in the long run, and its accelerating earnings growth should help it sustain its recent momentum.

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

Nvidia:if you invested $1,000 when we doubled down in 2009,you’d have $352,417!*

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $44,855!*

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $451,759!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of January 6, 2025

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia and Snowflake. The Motley Fool recommends Gartner. The Motley Fool has a disclosure policy.

2 Artificial Intelligence (AI) Stocks That Could Go Parabolic was originally published by The Motley Fool

Alisha Hunter is a news writer for Credence Advisors-News. She's been writing for over a decade, and she has taught herself all the skills she needs to be successful in this role.

Alisha has written about everything from technology to fashion; she's even written an advice column for brides-to-be!

Alisha loves reading books and watching movies - she's currently working on a book club with her friends where they read one book each month together!